When the Tax Man Comes Straight for Your Bank Balance

Pakistan’s Federal Board of Revenue has bypassed the courts entirely — and taken millions straight from a citizen’s account. Here’s what happened, and why it matters.

The Federal Board of Revenue has once again landed at the centre of a storm — this time not for missing its revenue targets, but for hitting them in a way that has left legal experts and ordinary taxpayers deeply unsettled.

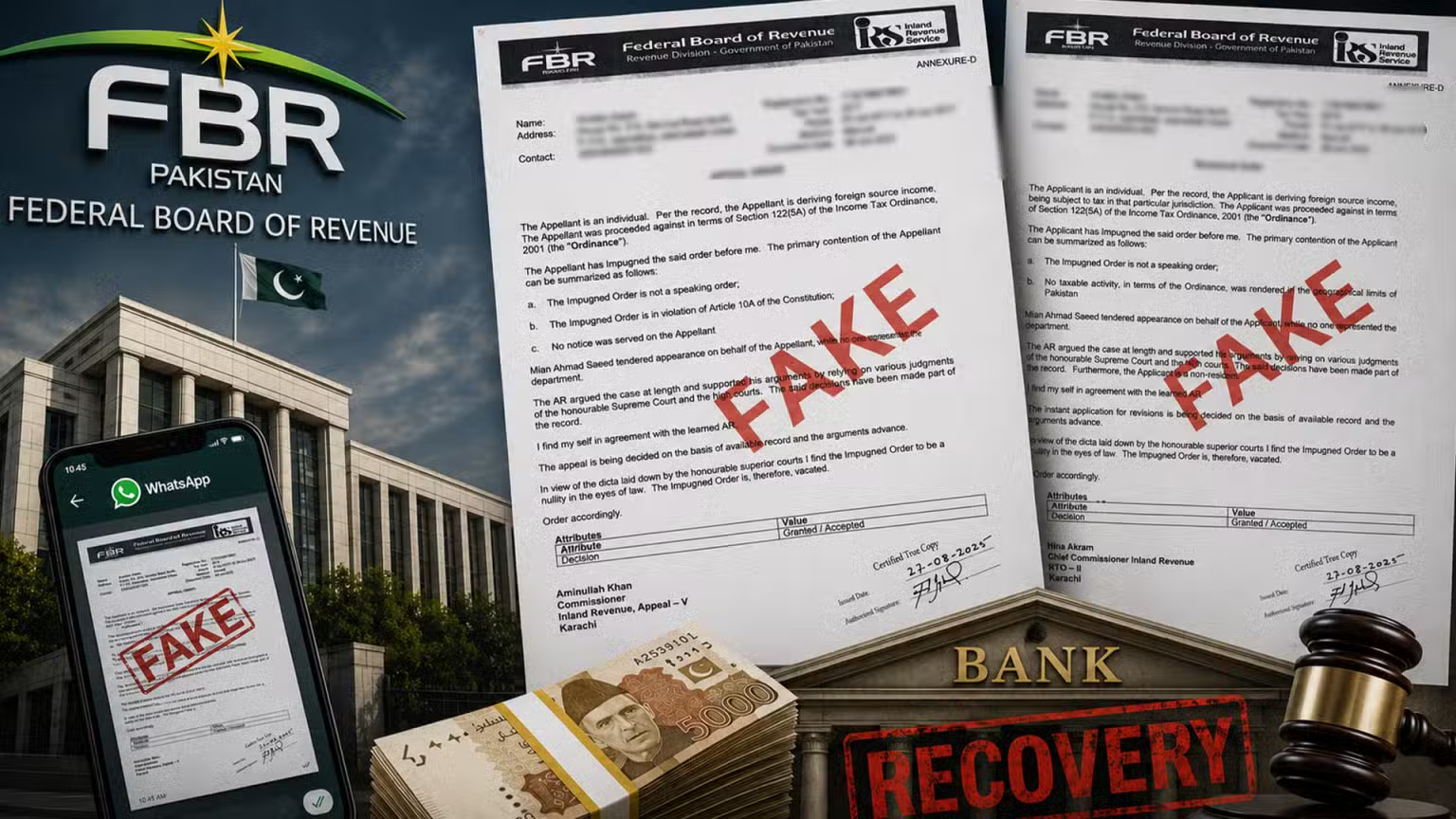

In a move that has sparked fierce debate across Pakistan’s financial and legal circles, the FBR directly recovered Rs. 3 crore from a private citizen’s bank account without going through the conventional court process.

The action, carried out under special provisions of the tax code, raises urgent questions about the limits of state power over personal finances.

What Exactly Did FBR Do?

The FBR bank account recovery was executed using the authority granted to the revenue body under Section 140 of the Income Tax Ordinance 2001 and corresponding provisions of the Sales Tax Act. These sections allow the FBR to issue a notice directly to a bank — without a court order — instructing it to debit a taxpayer’s account for outstanding dues.

In plain terms: the FBR did not sue the citizen in court. It did not wait for a judge’s approval. It went directly to the bank, handed over a recovery notice, and the bank transferred Rs. 3 crore out of the account.

According to sources familiar with the case, the taxpayer in question allegedly had long-standing outstanding dues that had not been cleared despite multiple notices. The FBR maintains that every procedural step was followed and that the recovery was entirely lawful.

A Power That Has Always Existed — But Rarely Used This Openly

This is not a new power. Tax authorities around the world have some version of it. In Pakistan, the FBR has held this authority for years. What makes this case notable is the scale — Rs. 3 crore is a significant sum — and the very public way in which the action has come to light.

Legal practitioners say the provision exists as a last resort, meant for cases where:

- The taxpayer has repeatedly ignored official notices

- There is clear and documented evidence of outstanding liability

- The amount owed is not under genuine legal dispute

- Alternative recovery avenues have already been exhausted

The problem, critics argue, is that these guardrails are not always respected in practice.

“It Sets a Dangerous Precedent,” Say Legal Experts

Lawyers and chartered accountants speaking to journalists this week were unanimous on one point: the legal authority may exist, but its use without adequate judicial oversight is alarming.

“The existence of a law does not automatically make every action under it just,” said one Lahore-based tax attorney who requested anonymity. “When you can go straight to a bank and remove someone’s money, you are exercising a power that courts themselves are normally required to exercise. That is a serious matter.”

The concern is not hypothetical. In several past cases, taxpayers have later proven — through appeals tribunals and courts — that the FBR’s demand itself was inflated, miscalculated, or based on flawed assessment. In those cases, recovering money from a bank account first and correcting the error later means the citizen bore an unjust financial burden for months or even years during the appeal process.

The Taxpayer’s Side of the Story

Details about the specific individual in this case remain limited due to privacy considerations, but what is known points to a dispute that had been simmering for some time.

The taxpayer reportedly argued that the assessed amount did not accurately reflect their actual tax liability and had intended to pursue the matter through formal appeal channels.

READ MORE: SECP Barwaqt and UdharPaisa Notice: How to Settle Your Loan Now

The FBR, however, moved ahead with direct recovery — a decision that leaves the taxpayer in the difficult position of having already lost the money and now needing to fight for its return.

Under Pakistani tax law, a person from whom money has been recovered this way can still file an appeal. But the burden of proof now sits entirely with them, and the process can stretch over months, during which their funds remain with the state.

How the FBR Bank Account Recovery Process Actually Works

For readers unfamiliar with how this works in practice, here is a step-by-step breakdown:

- Demand Notice Issued: FBR sends a formal notice of tax demand to the taxpayer.

- Non-Compliance Observed: If the taxpayer does not pay or respond adequately within the stipulated period, FBR escalates.

- Notice to Bank: FBR serves a notice directly to the taxpayer’s bank under Section 140 or equivalent provisions.

- Bank Complies: The bank is legally obligated to freeze and transfer the specified amount to FBR within a set timeframe.

- Taxpayer Notified: The taxpayer is informed — often after the fact.

- Appeal Window Remains Open: The taxpayer can challenge the demand at an appellate tribunal, though they must do so with the money already gone.

This process requires no court involvement at any stage. That is the crux of the controversy.

FBR’s Defence: “We Follow Due Process”

The FBR, for its part, has defended the action firmly. Officials insist that the agency does not initiate direct bank recovery lightly and that cases reaching this stage have invariably gone through multiple rounds of notice and non-response.

“We are mandated by law to recover taxes owed to the state,” a spokesperson indicated in comments to the press. “Where taxpayers refuse to engage despite lawful notices, we are left with no alternative but to use the legal tools available to us.”

The FBR is also under intense pressure from the government and the International Monetary Fund to broaden Pakistan’s notoriously narrow tax base and improve collection efficiency. In that context, direct recovery actions are likely to increase — not decrease — in the months ahead.

What This Means for Ordinary Pakistanis

For the average salaried person or small business owner, this story lands with an uncomfortable thud. Most people already have a difficult relationship with the FBR whether it’s the complexity of filing returns, confusion over notices, or fear of arbitrary demands. The idea that money can be taken directly from a bank account without a court order only deepens that anxiety.

Tax experts are urging citizens to take the following steps to protect themselves:

- Keep all tax filings current. Even if you believe you owe nothing, an unfiled return invites scrutiny.

- Respond promptly to any FBR notice. Silence is the worst possible response.

- Consult a tax professional if you receive any demand notice — especially before the response deadline.

- Do not ignore letters from your bank regarding third-party instructions. These can be the first sign of a recovery action underway.

- Know your appeal rights. The appellate tribunal system exists for exactly these situations, and you have the right to use it.

Is Reform Needed? Many Say Yes

The broader conversation triggered by this case is about whether Pakistan’s tax recovery framework strikes the right balance between state authority and citizen protection.

Several legal reform advocates have long argued that direct bank recovery without at least a fast-track judicial confirmation is incompatible with basic due process principles.

In countries like the UK, even HMRC’s direct recovery powers introduced in 2015 faced significant parliamentary scrutiny and were constrained by safeguards including a minimum balance protection, prior independent review, and the right to a face-to-face meeting before deduction.

Pakistan’s framework currently lacks several of these safeguards. Whether this case prompts legislative debate on the issue remains to be seen.

A Rs. 3 Crore Wake-Up Call

The FBR bank account recovery of Rs. 3 crore from a private citizen is not just a tax story. It is a story about power — who has it, how it is used, and what recourse ordinary people have when the state comes for their money without a judge’s say-so.

Whether the FBR acted within the bounds of law is, by most accounts, likely yes. Whether that law itself is adequate to protect taxpayer rights is a far more open question — and one that Pakistan’s legislature, civil society, and legal community would do well to take up before this becomes a pattern rather than an exception.

Have you received a tax notice from the FBR or been affected by a similar recovery action? Share your experience in the comments below — your story could matter to others facing the same situation.