Pakistan Lost Over $1.8 Billion to Foreign Profit Outflows in 9 Months

Pakistan Foreign Profit Outflows picture has taken a complicated turn. According to the latest data from the State Bank of Pakistan (SBP), foreign investors took out over $1.828 billion in profits and dividends during the first nine months of the current fiscal year — that is, from July 2025 to March 2026. That figure is $110 million higher than the same period last year, and it comes at a time when the inflow side of the equation is shrinking.

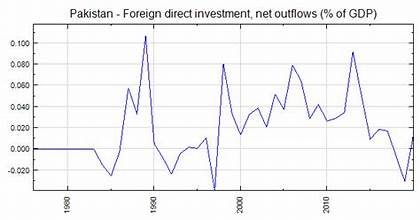

The numbers paint a picture that economists have been watching closely. On one hand, the rising repatriation signals that multinational companies are earning real returns in Pakistan — a sign of business confidence of a certain kind. On the other hand, with fresh foreign direct investment falling by nearly 27 percent over the same stretch, the net impact on the country’s external account is a cause for concern.

Where did the money go — and who took it?

The bulk of the outflows, around $1.76 billion, was tied to profits on foreign direct investment. Portfolio investment outflows made up the remainder. When you break it down by sector, two industries dominate the picture.

Sector | Outflow (Jul–Mar FY26) |

|---|---|

| Power / Energy | ~$422 million |

| Financial Business | ~$374 million |

| Food Sector | ~$142 million |

| Communications | ~$132 million |

| Transport | ~$91 million |

The power sector has consistently led profit outflows over recent years, a direct result of the large-scale investment deals — particularly under CPEC — that gave foreign energy companies long-term, dollar-denominated return guarantees. As those plants generate revenue, the profits flow back home.

On a country basis, investors from the United Kingdom walked away with the largest share of repatriated earnings — over $444 million during the nine-month period, though this was slightly lower than last year. China came in second with $413 million, a jump driven largely by energy-sector earnings. The Netherlands and the United States were also among the top recipients.

Country | Repatriated profits (approx.) |

|---|---|

| United Kingdom | $444 million |

| China | $413 million |

| Netherlands | $151 million |

| United States | $146 million |

Not just profits — treasury bonds are bleeding too

The foreign investment outflow Pakistan FY26 story doesn’t stop at FDI profits. A separate and more alarming trend has emerged in the government securities market. According to the SBP’s own data, nearly 90 percent of the foreign investment that had entered Pakistan’s treasury bills has now been withdrawn.

Total foreign inflows into government securities stood at $886.7 million during the first three quarters of the current fiscal year. Against that, withdrawals reached $794 million — leaving barely $93 million still parked in T-bills. In March alone, $227 million exited treasury bills while fresh inflows amounted to just $19 million.

The largest single withdrawal — $281 million — was repatriated to the United Kingdom. Investors from the UAE pulled out $209 million, followed by Bahrain at $170 million and Singapore at $77.6 million.

This is happening even though Pakistan’s treasury bill yields are sitting at an attractive 11.5 percent — a rate that would normally draw portfolio investors in. But the ongoing military tensions in the Middle East have cast a shadow over the region, making even high-yield instruments less appealing to risk-averse foreign capital.

Why is foreign investment leaving Pakistan?

There isn’t one single reason — it’s a combination of factors that have been building over time.

Interest rate cuts making T-bills less attractive

The State Bank of Pakistan has been cutting its benchmark interest rate aggressively — from a peak of 22 percent all the way down to 11 percent. That is an 11 percentage-point reduction in roughly two years. As rates fall, so does the appeal of fixed-income securities for foreign investors chasing yield. The math simply doesn’t work as well as it did before.

Geopolitical pressures and the Gulf conflict

The renewed military tensions in the Middle East have hit investor sentiment across the region, and Pakistan has not been immune. Higher oil and gas import prices are feeding domestic inflation, export markets in the Gulf have been disrupted, and the overall sense of regional uncertainty is pushing cautious investors toward safer markets.

Rupee depreciation risk

Concerns about the gradual weakening of the Pakistani rupee have also played a role. For a foreign investor, even a well-performing local investment can lose value once you convert profits back into dollars or pounds. That currency risk eats into returns and has been a persistent deterrent.

Political and structural uncertainty

Pakistan’s business environment continues to rank poorly in global indices. Red tape, inconsistent policy implementation, and a history of macroeconomic crises have made foreign investors cautious about committing long-term capital. The recent Pakistan-India tensions in May added another layer of uncertainty, further rattling investor confidence.

- Pakistan ranked 150th out of 184 countries on the latest investment index

- Net foreign portfolio outflows have exceeded inflows by 2,569 percent since 2014

- The telecom sector alone recorded $431 million in outflows in 2025 due to major divestments

- Total foreign investment for July–December 2025 stood at just $207 million — versus $1.3 billion in the same period a year earlier

A closer look at what’s actually working in Pakistan’s investment story

The very fact that foreign companies are repatriating large profits means they are making money in Pakistan. That is not a trivial point. A country where businesses cannot earn and freely transfer their earnings abroad is far less attractive than one where they can.

Earlier in the fiscal year, the sharp rise in profit repatriation — up 85.83 percent in the first quarter of FY26 alone — was partly attributed to the SBP’s more relaxed stance on capital outflows, in line with IMF recommendations. After years of informal restrictions that blocked MNCs from sending earnings home, the central bank normalized the process. So some of what we are seeing now is a catch-up of profits that had been queued up for months.

On the inflows side, China remains the single largest source of FDI, investing $583 million in 2025. The Roshan Digital Account program has crossed $12 billion in total inflows, reflecting that the Pakistani diaspora continues to engage with the country’s financial system.

And Pakistan’s foreign exchange reserves have climbed significantly from the $4.4 billion crisis-level lows of June 2023 to over $16 billion today.

The IMF’s $7 billion loan program, approved under the current government, is still on track — and a recent $1.02 billion tranche disbursement pushed Pakistan’s forex reserves above $11 billion earlier in the fiscal year.

Why Pakistan Foreign Profit Outflows Are Increasing

The pattern of foreign investment outflow Pakistan FY26 reflects a structural tension that Islamabad has struggled to resolve for years: how to attract and retain international capital in an economy that carries high political risk and limited policy credibility.

Analysts have pointed out that the task now is to convert Pakistan’s recent macroeconomic stabilization into something more durable. Inflation is easing, the rupee has stabilized relative to its 2023 lows, and the stock market has seen remarkable gains. But none of that will stick if the investment climate does not fundamentally improve.

For Pakistan to stop being a market where foreign firms earn and leave — rather than one where they earn and reinvest — the government will need to address structural bottlenecks: energy costs, regulatory predictability, contract enforcement, and the long-running problem of political instability that makes five-year business plans feel like guesswork.

Final Thought!

Pakistan recorded over $1.828 billion in foreign profit and dividend outflows in the first nine months of FY2025-26, according to the State Bank. That is 26 percent higher than the same period last year. At the same time, new FDI has fallen by 27 percent, meaning the country is losing more than it is gaining from the foreign investment relationship right now.

The power and financial sectors lead the outflows. The UK and China are the largest recipients of repatriated earnings. And the government securities market has seen a near-complete exit of foreign portfolio investors — spooked by interest rate cuts, geopolitical tension, and currency risk.

Whether this becomes a long-term structural problem or a temporary correction will depend heavily on what happens next — with the IMF program, with regional stability, and with Pakistan’s own commitment to economic reform.