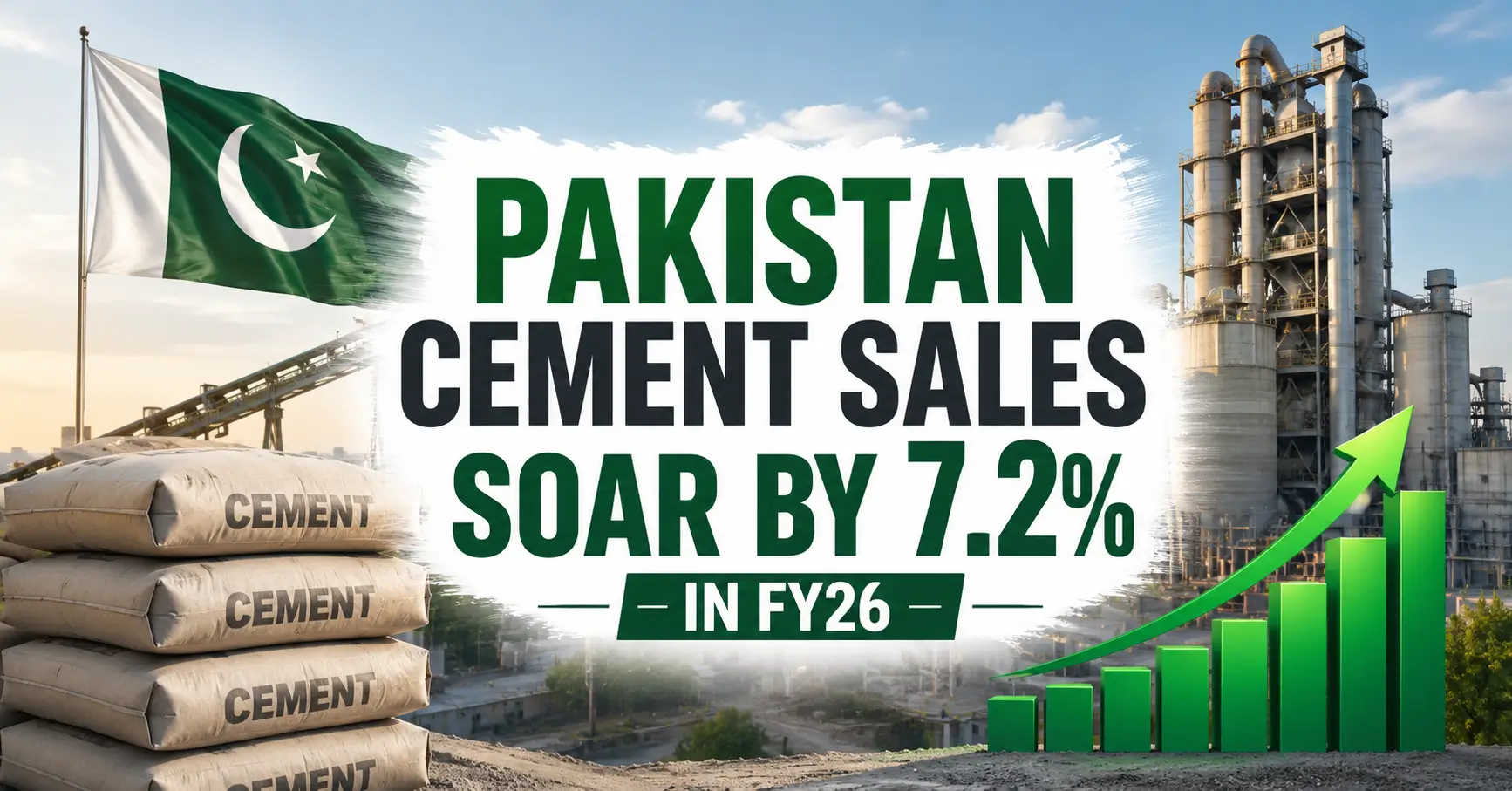

Pakistan’s cement industry just closed its strongest fiscal year in half a decade. Total dispatches climbed 7.21 percent to 50.52 million tons in FY26, and the numbers tell a story of a construction sector finally shaking off years of stagnation.

The recovery wasn’t driven by exports. It was driven by cranes, cement mixers, and rebar going up across the country.

The Numbers Behind the Rebound

Total cement dispatches increased by 7.21 percent, reaching 50.515 million tonnes against 47.116 million tonnes a year earlier, according to data released by the All Pakistan Cement Manufacturers Association (APCMA).

Break it down and the domestic story dominates. Local cement sales rose by 9.5 percent, climbing from 37.906 million tonnes in FY2024-25 to 41.507 million tonnes in FY2025-26. That’s the kind of jump construction-linked industries rarely see outside a genuine demand cycle.

Exports told a different tale. Export volumes fell by 2.19 percent to 9.008 million tonnes, compared to 9.210 million tonnes in the previous fiscal year. Nothing dramatic, but enough to show Pakistani manufacturers are increasingly selling at home rather than chasing overseas buyers.

READ MORE: Budget 2026–27: Cigarette FED Freeze Costs Pakistan Billions

June 2026 capped the year on a high note. Total cement dispatches surged 18.38 percent to 4.331 million tonnes, compared with 3.658 million tonnes in June 2025. Within that, domestic sales posted a sharp 26.78 percent increase, rising to 3.541 million tonnes from 2.793 million tonnes, while exports dropped 8.73 percent to 789,840 tonnes from 865,387 tonnes.

North vs South: A Tale of Two Cement Belts

Regional data shows the recovery wasn’t uniform. Northern mills sold 34.720 million tonnes domestically, an increase of 10.83 percent over 31.329 million tonnes in FY2024-25 — but their export book collapsed.

Exports from the region dropped sharply by 53.85 percent to 777,207 tonnes, down from 1.683 million tonnes, a sign that landlocked northern producers are losing ground in regional export markets as freight costs and competition bite.

Southern manufacturers played a different game entirely. Southern mills dispatched 6.787 million tonnes domestically during FY2025-26, up 3.18 percent from 6.577 million tonnes, while their coastal access let them push overseas.

Exports from the south grew 9.36 percent to 8.230 million tonnes, compared to 7.526 million tonnes a year earlier, pushing total dispatches to 15.017 million tonnes, a 6.48 percent increase.

The pattern is clear: south-based plants leaned on ports and export routes, north-based plants leaned almost entirely on domestic construction demand.

Why the Turnaround Happened

This isn’t a one-off spike. Analysts tracking the sector describe FY26 as part of a longer recovery arc. Total dispatches are estimated to reach just over 50 million tons for the year, growing 7 percent from FY25 and marking the second consecutive year of recovery after a prolonged downturn, according to Business Recorder’s BR Research.

The drivers are macroeconomic, not industry-specific. Pakistan’s construction cycle has been slowly stabilizing with easing inflation, reduced interest rates and better business confidence that revived private construction activity, which allowed domestic cement demand to recover from the depressed levels witnessed between FY22 and FY25.

Cheaper financing plus calmer prices gave developers room to restart stalled projects. Cement, being the first material ordered on any site, picked up the signal early.

Capacity Still Outpaces Demand

Here’s the catch nobody in the industry is celebrating too loudly: production capacity has grown even faster than sales.

The cement industry in Pakistan has witnessed a substantial increase in production capacity over the years, rising from 45.62 million tons in FY16 to 84.58 million tons in FY26.

Even with FY26’s strong dispatch numbers, capacity utilisation increased notably to 60.2 percent in FY26, from 55.1 percent last year — meaning nearly 40 percent of installed capacity still sits idle.

Business analysis flags the same imbalance directly: total dispatches remain well below the levels producers had envisioned when they embarked on an aggressive expansion drive several years ago, and installed capacity has continued to grow while consumption has struggled to keep pace, leaving the industry with one of the largest excess-capacity overhangs in the region.

That overcapacity keeps pricing power in check even as volumes rise, which is good news for buyers and a persistent headache for producers’ margins.

Exports Face Structural Headwinds

The export slowdown isn’t a blip either. Export dispatches are expected to decline this year as regional competition intensifies and freight economics become less favorable, particularly for southern manufacturers shipping through sea routes.

There’s a commercial logic pulling manufacturers homeward regardless. The shift back toward domestic sales is commercially better for producers, since local markets generally offer stronger pricing power and significantly lower logistics costs than exports.

But that comfort comes with a risk: it leaves the industry’s fortunes increasingly tied to Pakistan’s own construction sector, where demand remains heavily dependent on government development spending and housing activity.

What APCMA Is Watching Next

The association itself is cautiously bullish. A spokesperson expressed confidence that cement demand will hold up across both local and international markets in the coming months, and pointed to easing geopolitical tensions as a potential relief valve for energy costs — a persistent drag on production economics for a fuel-intensive industry like cement.

Policy support is already on the table. New tax measures for construction and real estate announced in the 2027 budget, alongside a subsidized housing finance scheme, are being positioned to keep the domestic demand engine running into the new fiscal year.

The Bigger Picture

FY26 marks Pakistan cement’s clearest recovery signal since the post-pandemic slump. Domestic demand is doing the heavy lifting, capacity utilisation is climbing, and two consecutive years of growth suggest this isn’t a seasonal blip.

But excess capacity, a shrinking export base, and heavy reliance on government spending mean the industry’s next chapter depends less on how much cement gets made — and more on whether Pakistan’s construction boom has the legs to last.

Will Pakistan’s cement sector keep climbing in FY27, or is this recovery running out of road?