Crude Reality: Oil Prices Are Sliding Toward a 2-Year Low — And Nobody’s Hitting the Brakes

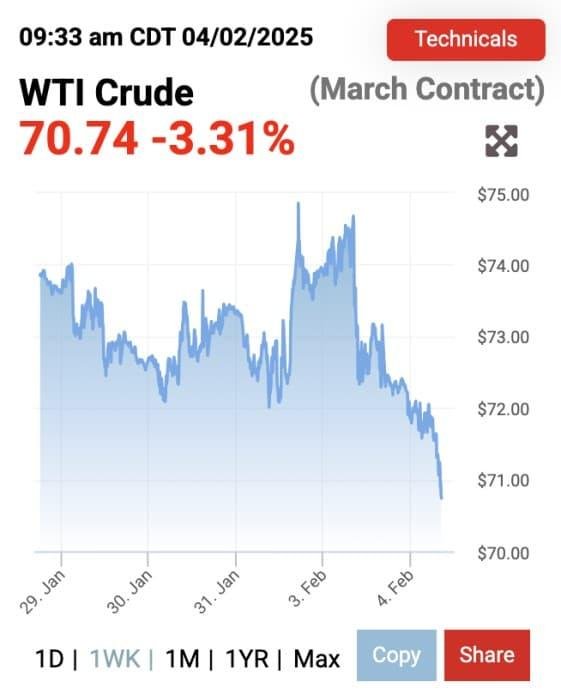

Oil hasn’t looked this cheap in a long time. After months of pressure building beneath the surface, crude prices are now teetering on the edge of falling below $70 per barrel — a level not seen in nearly two years. Analysts, traders, and energy ministers are all watching the same thing: a market that’s losing its footing fast, and a global economy that may not be strong enough to catch it.

Why Oil Prices Are Approaching a Two-Year Low

The global oil market has been under pressure for several months, but the slide toward the $70 threshold has gathered pace in recent weeks. Brent crude — the international benchmark — has been hovering in the low-to-mid $70s, with traders increasingly pricing in a further decline. West Texas Intermediate (WTI), the US benchmark, is tracking a similar trajectory.

So what’s actually behind this? It’s not one thing — it rarely is with oil. It’s a combination of oversupply concerns, weakening demand signals from major economies, and a strategic shift by OPEC+ that has surprised even seasoned market watchers.

The numbers are stark. At its recent lows, Brent crude has touched levels that, if sustained, would represent the lowest oil prices since the summer of 2023. For an energy market that was still celebrating post-pandemic recovery just 18 months ago, this is a significant reversal.

OPEC+ Loosens the Tap — And Markets React

One of the biggest drivers of the current slide is a decision by OPEC+ — the alliance of major oil-producing nations led by Saudi Arabia and Russia — to gradually unwind production cuts that had been propping up prices.

The group had maintained tight supply discipline since late 2022, keeping barrels off the market to support prices above $80. That strategy worked — until it didn’t. With some member states reportedly exceeding their quotas and non-OPEC producers like the United States continuing to pump at elevated levels, the cartel’s grip on supply has loosened.

Earlier this year, OPEC+ agreed to increase output in a phased manner, signalling that the era of aggressive supply management may be drawing to a close. The message markets received was simple: more oil is coming, and prices need to adjust.

Saudi Arabia, in particular, appeared to send a pointed signal — it would no longer sacrifice market share to hold up prices at the expense of discipline from other members.

Demand Is the Other Half of the Problem

Supply alone doesn’t tell the full story. Demand is equally — if not more — responsible for where prices are heading.

China, which accounts for a significant share of global oil consumption, has delivered a series of disappointing economic data points this year. Its post-pandemic recovery has been slower and more uneven than expected, and consumer confidence remains fragile. Chinese crude imports, while still substantial, have not grown at the pace markets had anticipated.

Meanwhile, in Europe and the United States, economic momentum is slowing. The prolonged period of high interest rates — a consequence of central bank efforts to bring down inflation — has weighed on industrial activity and fuel demand. Manufacturing output in Germany, historically a bellwether for European economic health, has contracted for several consecutive months.

The picture that emerges is one where supply is rising and demand is softening. In any commodity market, that’s a recipe for falling prices.

What $70 Oil Actually Means

The $70-per-barrel mark isn’t just a round number — it carries real significance for energy markets and government budgets alike.

For oil-exporting nations:

- Saudi Arabia is widely estimated to need oil prices above $80 to balance its national budget. A sustained drop below $70 would create fiscal pressure and potentially force spending cuts or a drawdown of reserves.

- Russia, already under Western sanctions, faces similar budget arithmetic, with its fiscal breakeven price estimated in the $70–$80 range depending on the source and the year.

- Smaller producers in the Gulf and in Africa could face more acute strain, particularly those with limited sovereign wealth buffers.

For oil companies:

- Major integrated oil companies — BP, Shell, ExxonMobil, TotalEnergies — can generally remain profitable at $70, but exploration budgets and capital expenditure are likely to come under review.

- Smaller independent producers and shale operators in the US, where breakeven costs vary widely, could find margins tightening significantly.

For consumers and businesses:

- Lower oil prices typically feed through to cheaper petrol at the pump, reduced energy bills, and lower costs for goods that rely on transportation and manufacturing.

- For inflation-weary households across the UK, Europe, and beyond, cheaper oil is broadly welcome news — at least in the short term.

The US Shale Factor

American oil production has been a persistent wildcard in global energy markets for over a decade, and this cycle is no different. US crude output has remained near record highs, adding to the supply glut that is pushing oil prices lower.

READ MORE: Pakistan Slashes Petrol Price by Rs. 74 Per Litre

The shale industry, once seen as highly sensitive to price swings, has become more resilient over time as operators have cut costs and improved efficiency. Many producers in the Permian Basin — the most productive oil field in the United States — are still generating positive cash flow at prices well below $70, which means there’s little incentive to cut production even as prices slide.

This dynamic complicates OPEC+’s calculations significantly. Every barrel of American crude that enters the market dilutes the effect of any supply discipline the cartel tries to enforce.

Could Oil Fall Even Further?

The short answer: possibly, yes.

Several analysts have revised their price forecasts downward in recent weeks. Goldman Sachs, among others, has flagged the possibility of oil prices dipping into the $60s if demand disappoints further or if OPEC+ adds more supply than the market can absorb.

A scenario where oil prices fall to $60–$65 per barrel would be a significant shift in the energy landscape — one that would accelerate budget reviews, investment cuts, and potentially a reassessment of the clean energy transition timeline in some markets.

However, markets rarely move in straight lines. There are factors that could slow or reverse the decline:

- Geopolitical risk: Tensions in the Middle East, Africa, or between Russia and the West can rapidly tighten supply expectations and push prices higher.

- OPEC+ response: If prices fall sharply enough, the alliance could reverse course and reimpose production cuts — though doing so credibly after recent decisions would require consensus that has proven elusive.

- Seasonal demand: Summer driving season in the Northern Hemisphere and increased air travel activity typically provide a lift to fuel demand in the third quarter.

None of these factors are guaranteed, but they represent real counterweights to the bearish trend.

What Energy Analysts Are Watching

Traders and energy economists are closely monitoring several indicators in the coming weeks:

- US crude inventory data — Weekly figures from the Energy Information Administration (EIA) can move markets sharply if they show surprise builds or drawdowns.

- Chinese import data — Any sign of a pickup in Chinese buying activity would provide a demand floor that the market currently lacks.

- OPEC+ meetings and communications — Any signal of a policy reversal could stabilize prices quickly.

- Macroeconomic data from the US and Europe — Stronger-than-expected growth figures could revive demand optimism.

Until those signals shift, the path of least resistance for oil prices appears to be downward.

What This Means for the UK and British Energy Bills

For British households and businesses, the prospect of oil prices falling below $70 carries both direct and indirect implications.

Lower crude prices typically feed into reduced petrol and diesel costs within a few weeks, though the pass-through is not always immediate or complete — taxes make up a large portion of pump prices in the UK, which limits the consumer benefit somewhat.

Gas prices, which are more closely tied to European natural gas markets than to crude oil directly, may see a more indirect effect. However, if energy commodity prices fall broadly, wholesale electricity and heating costs could ease over time.

The broader economic picture is also relevant. Cheaper energy reduces operating costs for businesses, which can help moderate inflation — a consideration that will not be lost on the Bank of England as it assesses its interest rate path in the coming months.

Final Thought: A Market in Motion, A Price Under Pressure

Oil prices falling below $70 for the first time in nearly two years would mark a meaningful shift in the global energy landscape. It reflects a market caught between an OPEC+ alliance struggling to maintain discipline, a global economy running below its potential, and a structural supply surge that shows no sign of stopping.

For now, the trend is clear. Whether $70 holds as a floor — or becomes the ceiling of the next leg lower — will depend on decisions made in Riyadh, Beijing, and Washington over the coming weeks and months.

One thing is certain: the days of easy, high oil prices that producers enjoyed in 2022 and 2023 feel increasingly distant.

What do you think falling oil prices mean for energy costs where you live? Share your views in the comments below.